product

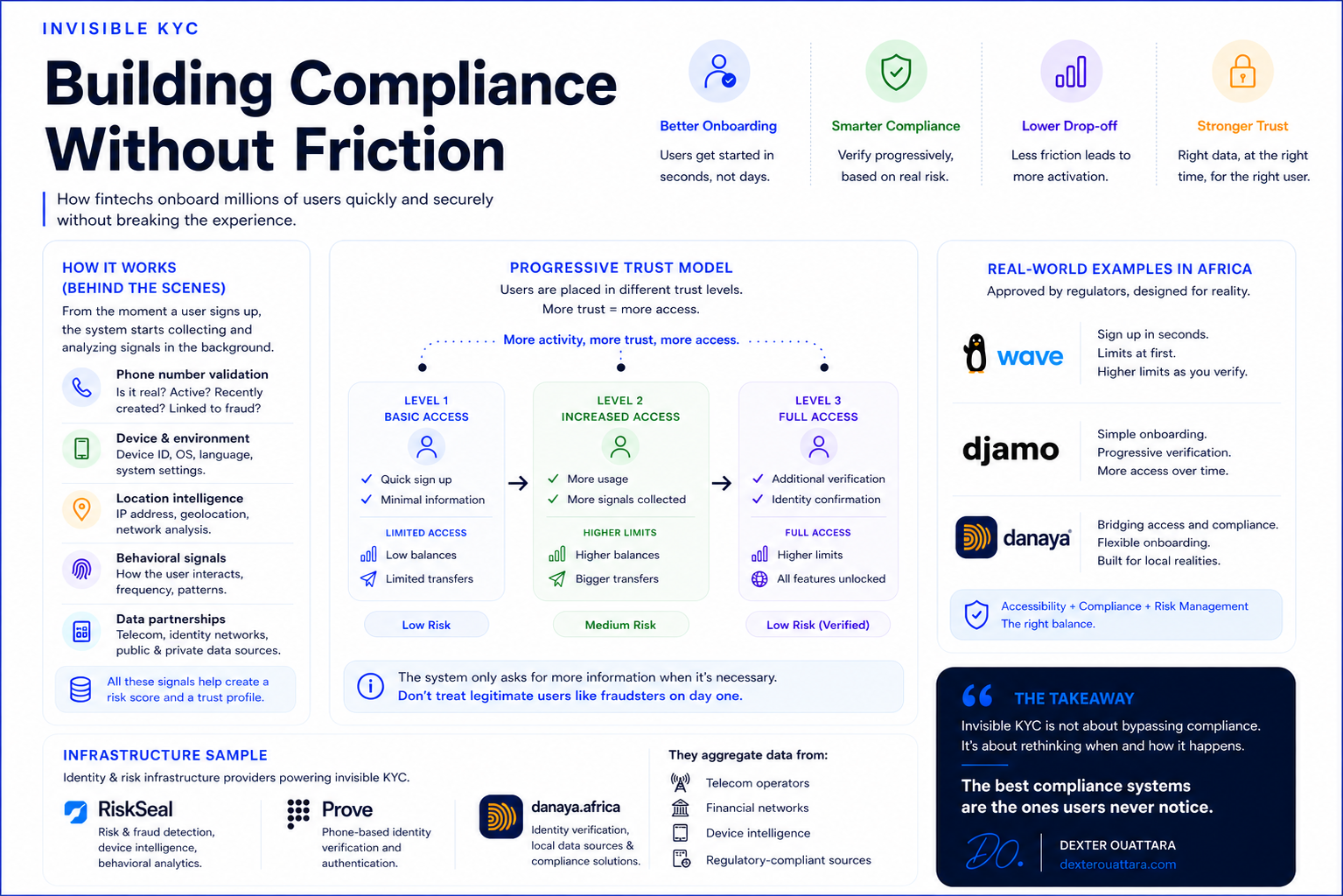

Invisible KYC: Building Compliance Without Friction

When we started exploring Codeln Pay,

a way to help engineers access global wallets and get paid internationally, one question came up immediately:

How do you stay compliant without breaking the user experience?

Because in fintech, compliance is not optional.

But friction kills adoption.

That’s where the concept of Invisible KYC becomes critical.

What is Invisible KYC?

Think about the last time you signed up for a financial app.

You entered your phone number or email…

and within seconds, you could already:

- access the app

- explore features

- sometimes even send money

Compare that to traditional banking where onboarding can take days.

That difference is not accidental. It’s the result of Invisible KYC.

How it works (behind the scenes)

Instead of asking everything upfront, modern systems collect and verify data progressively.

From the moment you sign up, the system starts building your profile using signals like:

- phone number validity

- device information

- IP address and location

- language and system settings

- behavioral patterns

It also checks:

- if the number is real or virtual

- if it’s newly created

- if it’s linked to known fraud patterns

In many markets, phone numbers are tied (directly or indirectly) to identity systems via telecom operators or specialized data providers.

Even without asking for your ID immediately,

the system already has a level of confidence about who you are.

Progressive trust: not all users are treated the same

Invisible KYC works by placing users into different trust levels.

At the beginning:

- you get basic access

- limited permissions

- capped transaction amounts

As your activity evolves:

- the system gathers more signals

- flags potential risks

- and requests additional verification when needed

You only get asked for more information when it becomes necessary.

This is the key idea:

Don’t treat legitimate users like fraudsters on day one.

Real-world examples in Africa

This model is already widely used and approved by regulators in markets like Côte d’Ivoire.

Products like Wave and Djamo in Abidjan follow this approach:

- you can sign up quickly with minimal information

- you get immediate access to core features

- but your transactions are limited at the beginning

As you:

- increase usage

- request higher limits

- or perform certain actions

the system progressively asks for more verification.

This creates a balance between:

- accessibility

- compliance

- and risk management

The infrastructure behind it

This experience is powered by a growing ecosystem of identity and risk infrastructure providers.

Companies like:

- RiskSeal

- Prove

- Danaya (danaya.africa)

…offer APIs and services that allow fintechs to:

- verify phone numbers

- assess fraud risk

- analyze device and behavioral signals

- access local identity and compliance layers

These systems aggregate data from:

- telecom operators

- financial networks

- device intelligence

- regulatory compliant data sources

The goal is simple: increase trust without increasing friction.

Why this matters for Africa

In African markets, this approach is not just useful, it’s necessary.

Because:

- identity systems are fragmented

- access to documentation can be limited

- infrastructure is uneven

If you introduce heavy KYC too early:

users drop before they even understand your product. Invisible KYC allows you to:

- onboard faster

- reduce friction

- adapt to local realities

- stay compliant progressively

The product challenge

As a Product Manager, your role is not just to solve problems.

It’s to solve them without breaking the experience.

Compliance is one of the hardest areas to get right because:

- it introduces friction

- it adds constraints

- it is driven by regulation

But the best products find the balance: maximum trust with minimum friction

A new standard for onboarding

In today’s competitive landscape, onboarding is no longer just a step.

It’s a core product experience.

To build it right, you need to:

- understand available infrastructure

- leverage third-party solutions

- design progressive trust systems

- think in terms of user experience, not just compliance

Because the reality is simple:

users don’t leave because of regulation

they leave because of friction

Invisible KYC is not about bypassing compliance. It’s about rethinking when and how it happens.

For companies building in complex environments like Africa, this is not just an optimization.It’s a competitive advantage.

Dexter Ouattara

Product Strategy & Entrepreneurship

Want to discuss your product strategy?

Book a consultation to get personalized insights for your business.

BOOK A CONSULTATION